Warren Buffet Closes His Fund in 1969

Warren Buffet Closes His Fund in 1969

In 1969 Warren Buffet starts liquidating his fund due to various reason we'll discuss. One aspect pops up - Warren Buffet cares about his investors and shows integrity when closing his fund.

In my last summary, I wrote about Warren Buffet’s Partnership fund he managed from 1957-1969. In 1969, Buffet announced that he’d close the fund for several reasons. Let’s start from the beginning.

Before you start here, I’d recommend reading my previous post - Warren Buffet - Shareholder Letters 1958 - 1968

Buffet’s Results and Market Deterioration

Already in 1967, Buffet mentioned that he was having a hard time in the stock market with rising speculative behavior and fewer and fewer undervalued companies that emerged within that environment.

In 1967, Buffet wrote the following:

Such statistical bargains have tended to disappear over the years… When the game is no longer being played your way, it is only human to say the new approach is all wrong, bound to lead to trouble, etc. I have been scornful of such behavior by others in the past. I have also seen the penalties incurred by those who evaluate conditions as they were – not as they are. Essentially I am out of step with present conditions. On one point, however, I am clear. I will not abandon a previous approach whose logic I understand (although I find it difficult to apply) even though it may mean foregoing large and apparently easy profits to embrace an approach which I don’t fully understand, I have not practiced successfully and which, possibly, could lead to substantial permanent loss of capital.

Buffet is probably one of the most humble investors out there, and he manages his investors’ expectations each and every year clearly. He states that the performance that his fund experienced over the last few years might not be attainable over the long run. That he is satisfied outperforming the Dow Jones Industrial Average at a rate of 10% instead of 22%.

What was his performance in 1970?

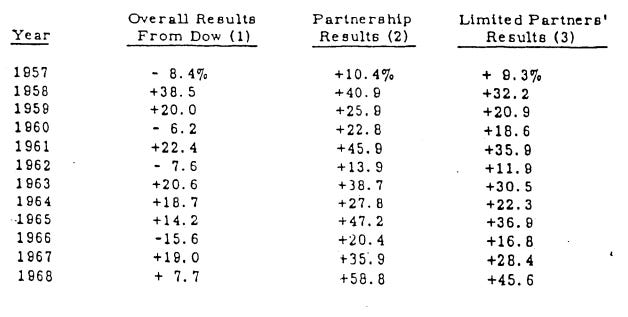

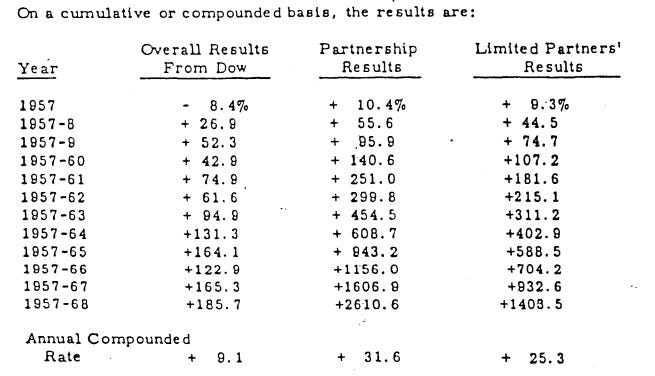

Let’s start with the YoY performance of his fund:

He had two partnerships. The first are those of the first few investors, like his family and friends. He then opened up a bit and created the Limited Partners.

Yes, you’re reading right. That’s an average 31.6% YoY return for the Partnership and 25.3% YoY for Limited Partners over 12 years! The Dow returned on average 9.1% YoY.

On an accumulated basis, Buffet returned 2610.6% for the Partnership and 1403.5% for Limited Partners over 12 years.

At the time, he wasn’t comfortable anymore within the market. A few trends emerged that he found highly question-worthy, like the chain-letter type stock-promotion vogue that emerged in the mid-sixties. He describes those participating as “gullible, self-hypnotized, cynical participants in this game.”

He sold many positions because they bloated up and made fantastic returns. But he mentions that his portfolio is starting to experience concentration and that value deals are few and far between. He started mentioning it in 1967, jokingly assuring that his statement back then was and still is true.

The Generals - Relatively Undervalued category - produced about two-thirds of the overall gain in 1966 and 1967 combined. I mentioned last year that the great two-year performance here had largely come from one idea. I also said, “We have nothing in this group remotely approaching the size or potential which formerly existed in this investment.” It gives me great pleasure to announce that this statement was absolutely correct. It gives me somewhat less pleasure to announce that it must be repeated this year.

Warren Buffet 1969

He continues:

I can’t emphasize too strongly that the quality and quantity of ideas is presently at an all time low - the products of the factors mentioned in the October 9th, 1967 letter, which have largely been intensified since then.

Warren Buffet 1969

So, what did the market look like around 1969?

His timing was marvelous. The feeling Buffet had at the time that there were no more bargains in the market coincides perfectly with the local high of the market at the time. He closed his fund in October 1969 and retired from investing for a short time. In 1970, the market deteriorated immensely, and in 1971 the Gold Standard was broken, leading to double-digit inflation and a short-term market crash.

Despite Warren Buffet’s immense returns, he rather liquidates the fund than hold it in a market where he sees no bargains.

He did because of his one crucial characteristic: Integrity

Learnings from his decision to end the fund

There are a few key learnings that we can take with us. First and foremost, when Warren Buffet says that he feels the market is overvalued and contains few to no bargains, even he will pull himself back. He’d rather not invest than start speculating.

At the time of closing the fund, 90% of Buffet’s wealth was in the fund. He was one of the largest principals and an agent. Other large investors were his family and closest friends, making it important to him to act in their best interest.

After 12 remarkable years of success, Warren Buffet remains humble, and it feels like he suffers from a bit of imposter syndrome, which led him to close the fund.

The imposter syndrome is not a negative statement. High-performance athletes often experience some impostor syndrome, leading them to become ever so slightly better. Many people with imposter syndrome attribute their accomplishments to luck rather than ability (like Warren Buffet does continuously) and fear that others will eventually unmask them as fraud. This syndrome is one reason they urge to improve, learn more, and question themselves.

Well, that’s just a theory. Take it with a grain of salt. Warren Buffet probably knows that he is a good investor. He has a specific investment style that worked for him and continues to stick to it.

At the peak of the speculative mania, he mentions the following:

I am not attuned to this market environment, and I don’t want to spoil a decent record by trying to play a game I don’t understand just so I can go out a hero

Warren Buffet 1970

Summary and Key Learnings

We can learn a lot from Warren Buffet. His writings are filled with wisdom. Many of the topics he discusses apply not only to investing but to life as well.

Key Lessons about Investing are:

The great thing about the stock market is - you don’t have to invest if you don’t find bargains.

Holding cash is a viable alternative to holding stocks and can sometimes generate superior returns.

Don’t fall for get-rich-quick schemes - no matter the time

Get-rich-quick schemes have probably always existed - Ponzi, Snakeoil, Real Estate 2007, Internet Bubble, Tulip Mania… The list goes on.

There is no shortcut to a thorough and intellectual analysis to generate long-term results.

Invest for the long term - ignore short-term price movements.

One of the best statements he makes is, “Price is what you pay, value is what you get.” I think about this statement a lot and realize just how true it is. The market throws prices at you in millisecond intervals. You can accept or reject them. Your job is to evaluate the underlying business and calculate its worth in relation to outstanding shares.

Companies and their stock will prosper or suffer, in the long term, in relation to the operating performances of their business.

If you got this far, thank you for reading my newsletter! If you were able to learn anything, really anything, please let me know in the comments.

I would also highly appreciate it if you could share this article, and if you haven’t done so already, subscribe.