Warren Buffet - Shareholder Letters 1958 - 1968

Warren Buffet - Shareholder Letters 1958 - 1968

Warren Buffet is one of the best investors of the last century, outperforming the market indices over any 5-year period by a wide margin. We can learn a lot from his shareholder letters!

I love writing on Substack and sharing knowledge with others. If you learn anything from this article, I would highly appreciate it if you would subscribe and share it with others!

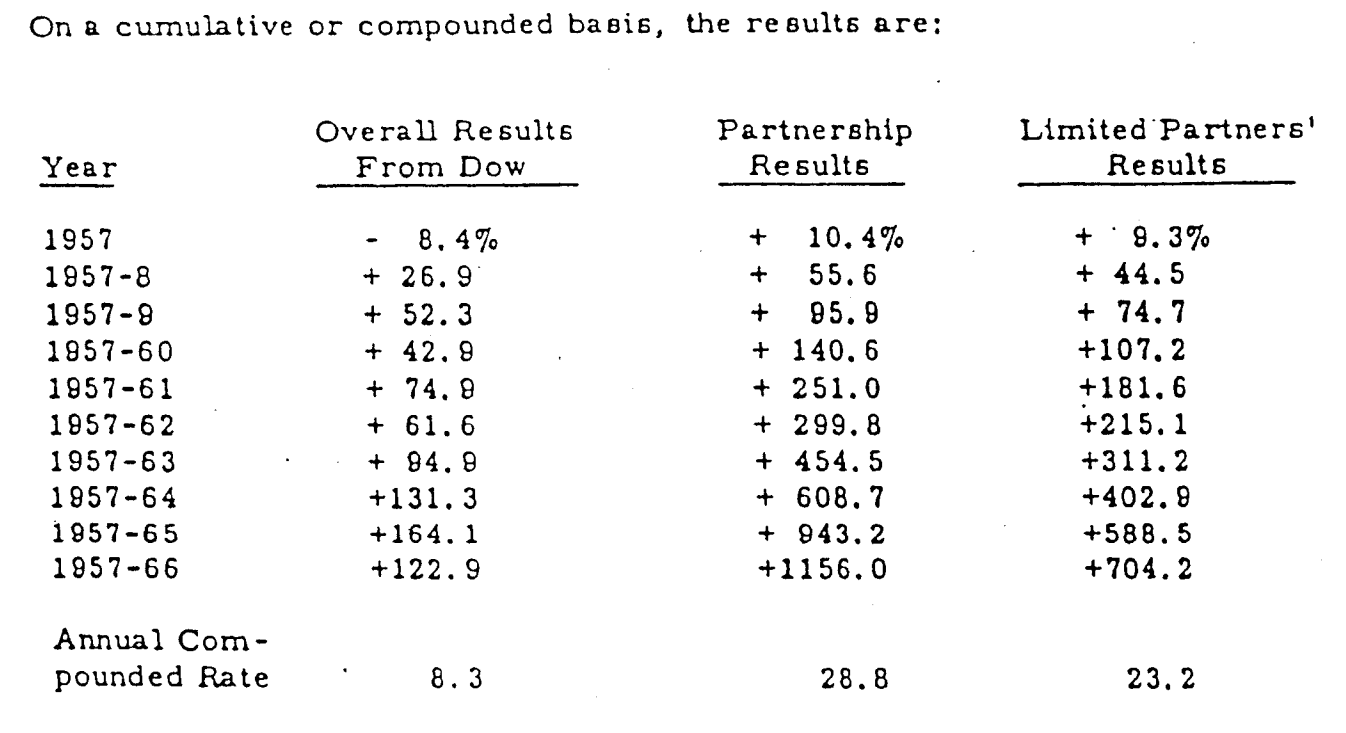

In the first 10 years, Warren Buffet and his Partnership outperformed the Dow Jones Industrial Average by a mere 20.5% on a compounded basis.

I’m being a bit ironic here because the results are insane, and any other investor that can mimic his results over a 10-year period would be considered a genius investor.

His shareholder letters are an iconic source of knowledge as he discusses his investment philosophy and psychological requirements to be successful in markets. Let's dig in!

Shareholder Letters 1957-1961

During this timeframe, the market was flooded with new professional and amateur traders that started speculating and pushing valuations higher. Mr. Buffet is not interested in speculation and keeps away from stocks that are popular with the masses.

I make no attempt to forecast the general market - my efforts are devoted to finding undervalued securities. However, I do believe that widespread public belief in the inevitability of profits from investment in stocks will lead to eventual trouble. Should this occur, prices, but not intrinsic values in my opinion, of even undervalued securities can be expected to be substantially affected.

Warren Buffet - Shareholder letter 1959

So much wisdom in this little quote. Following Benjamin Graham’s steps, the market can stay irrational longer than you can stay solvent. Even undervalued stocks - stocks that trade below intrinsic value - can still trade lower in speculative market environments.

He emphasizes the core investment philosophy and his competitive advantage against the general market.

He doesn’t try to outperform the market in a bull market

He considers a year in which his fund declines 15% less than the Dow Jones superior to a year in which both advance 20%. Let that sink in!

His competitive advantage lies in investing in businesses that trade below intrinsic value and outperform the market in stable and downward trends.

Mr. Buffet outperforms when the market is in distress while matching or outperforming when the market booms.

When he finds an opportunity, he makes sizeable bets that can reach 10-20% of his fund’s total assets.

He is not in a hurry to invest. In a bull market, few stocks are trading at a discount. A good investor keeps searching when no opportunity prevails.

During bull markets, market participants often talk about a new era of investment and valuation. Participants persuade each other that valuation reached a constantly higher level than in the previous era. Buffet’s answer to this is:

Perhaps other standards of valuation are evolving which will permanently replace the old standards. I don’t think so. I may very well be wrong; however, I would rather sustain the penalties resulting from over-conservatism than face the consequences of error, perhaps with permanent capital loss, resulting from the adoption of a “New Era” philosophy where trees really do grow to the sky.

Warren Buffet - 1960

Buffet’s partners ask him how he can outperform the market and even other funds - his response is that

Invest in low-risk and high-uncertainty businesses

If you’re buying what everyone else is buying, you cannot expect to outperform the average. You are the average.

To the extent that this is true, it indicates that our portfolio may be more conservatively, although decidedly less conventionally, invested than if we owned “blue-chip” securities. During a strongly rising market for the latter, we might have real difficulty in matching their performance.

Warren Buffet - 1961

Shareholder Letters 1962-1965

An investor must have a long-term mindset. One year is far too short of forming any kind of opinion as to investment performance. He has always been reluctant to write semi-annual letters to prevent his partners from starting to think in even shorter intervals. His thinking is geared towards at least five-year intervals, including different stock market environments (bull, bear, stagnant.)

He invests primarily in four categories:

Undervalued securities - Generals - Private Owner Basis:

Invest in undervalued businesses on a qualitative basis (below intrinsic value).

Invest in good management - a decent industry - and in value.Undervalued securities - Generals - Relatively undervalued:

These are companies selling at relatively cheap prices compared to companies of the same quality or better and in similar industries. Apples must be compared to apples - that’s key in this category.

If the industry is too complicated or opaque, Mr. Buffet stays away from it.Work-out:

Here, Mr. Buffet needs to initiate corporate action rather than wait for market supply and demand to settle. These are securities with timetables that Mr. Buffet can predict.Control:

Here, Mr. Buffet takes control of the company to influence policies and the company. These types of investments take years to play out.

The last two categories might not be viable to smaller investors, yet they are interesting. The first two are at the core of value investors, finding stocks that trade below intrinsic value.

The Questions of Conservatism

Many investors and funds say they invest conservatively by investing in blue chips. That’s a huge misunderstanding.

Conscious, perhaps overly conscious, of inflation, many people now feel that they are behaving in a conservative manner by buying blue chip securities regardless of price-earnings ratios, dividend yields, etc. Without the benefit of hindsight as in the bond example, I feel this course of action is fraught with anger. There is nothing at all conservative, in my opinion, about speculating to just how high a multiplier a greedy and capricious public will put on earnings.

Warren Buffet - 1962

Valuation matters, and it matters a whole lot when we’re entering bear markets. If you’re following the masses, don’t expect different results than the average. If you invest in businesses with extraordinarily high valuation metrics and are priced for perfection, don’t be surprised when you lose most of your investment.

Now, this is one of Buffet’s best quotes thus far:

You will not be right simply because a large number of people momentarily agree with you. You will not be right simply because important people agree with you. You will be right, over the course of many transactions, if your hypotheses are correct, your facts are correct, and your reasoning is correct. True conservatism is only possible through knowledge and reason.

Warren Buffet - 1962

True conservatism is only possible through knowledge and reason! Let that sink in for a moment. He is telling us that without learning about the companies you’re investing in and establishing a valuation framework to determine their valuation, you can’t invest conservatively.

Even when Warren Buffet says something about a business, you can’t take his information for granted. You won’t simply be right when he agrees with you.

Do your research!

Compounding is the 8th world wonder.

Each year, Mr. Buffet talks about the power of compounding. How seemingly minuscule differences in compounding rates can lead to significant sums over a sufficiently long timeframe.

Stay invested for the long term. If you can’t beat the market, invest in an index. Let compounding work for you.

Investment principles

As value investors, it’s our job to find undervalued businesses so attractively priced that even mediocre sales give us good results.

Remain humble - even Warren Buffet expected his fund to return less than it did yearly.

Don’t invest in rumors! You don’t need to participate in each and every market hysteria.

Patience is key

Value investing is a long-term game.

Let your thesis play out for at least 2-3 years!!

Don’t expect glamour or being the big talk.

Value investing is a boring business with boring companies that no one knows. You won’t be able to talk about high-flying glamour stocks as a value investor.

Shareholder Letters 1966-1968

Are you investing conservatively or conventionally? Many investors set these term equal, but they’re fundamentally different.

It is unquestionably true that the investment companies have their money more conventionally invested than we do. To many people conventionality is indistinguishable from conservatism. In my view, this represents erroneous thinking. Neither a conventional nor an unconventional approach, per se, is conservative.

Warren Buffet - 1965

As mentioned above, conservative investing comes from careful thought, research, intelligent hypothesis, correct facts, and sound reasoning.

Investing is a lot about your psychological stability. If you can’t handle a 20-30% drop in the market value of your stocks, then investing in stocks is not the right vehicle for you.

If you can’t stand the hear, stay our of the kitchen.

Harry Truman

When investing or even in life, most errors occur by forgetting what one tries to do. Don’t try to “get even” on a security that has declined. Past performance is of no importance for your future research.

As a value or contrarian investor, your journey is often lonely and against the grain. Don’t let others or the markets dictate your actions. Your research and thesis determine if you will be right over 2-3 years.

We don’t buy and sell stocks based upon what other people think the stock market is going to do (I never have an opinion) but rather upon what we think the company is going to go. The course of the stock market will determine, to a great degree, when we will be right, but the accuracy of our analysis of the company will largely determine whether we will be right. In other words, we tend to concentrate on what should happen, not when it should happen.

Warren Buffet - 1967

Thank you

I hope you enjoyed the first part of a series of articles that try to extract the most important pieces from nearly 80 years of shareholder letters from the best investor of our time.

Feel free to share this article with others. Like and comments are highly appreciated!