The Most Powerful Force in the Stock Market

The Most Powerful Force in the Stock Market

Regression to the mean is the most powerful force in the stock market and generation after generation fall victim to its force. Learn how to cope and even benefits from the regression to the mean!

2021 wasn’t a normal year by any means. We experienced worldwide lockdowns, mask mandates in public places, a shutdown in travel, and logistical issues that aren’t resolved yet.

In 2021, investors poured money into the stock market that they would otherwise have spent on travel, leisure, or other activities. The lockdowns and a sudden burst in income - pandemic stimulus - led to an excessive capital flow in stocks. As has happened many times, optimism turned to euphoria and speculation. The stock market soared beyond what’s good and bad.

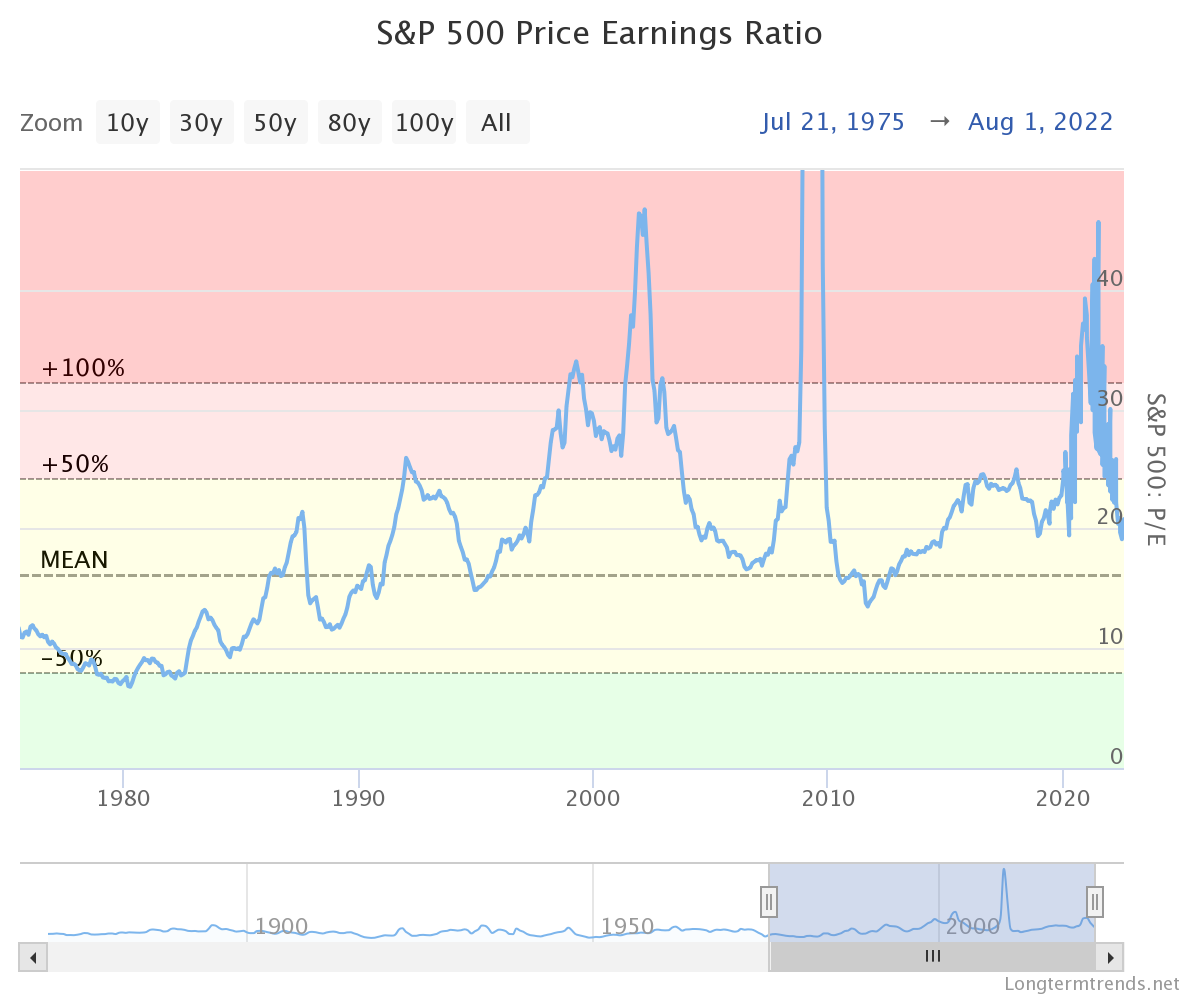

The chart below shows the price-to-earnings ratio for the S&P 500. There are three distinct peaks on this chart from 1975 to 2022.

The dot-com bubble around 2001

The global financial crisis - 2007-2008

Covid-19 Pandemic Mania 2021

Each period is characterized by heightened speculation, easy money, and easy credit. Each time people convinced each other that “this time is different.”

But it wasn’t.

Strong capital outflows and economic recessions followed each one of these peaks.

Aside from many other cognitive biases, one that seemingly everyone tends to forget when the market soars is the reversion to the mean.

Regression to the Mean

Statisticians have known the concept of regression to the mean for centuries. Mathematician Sir Francis Galton first discovered the concept of the regression to the mean in the 19th century.

The definition of the regression to the mean is as follows:

When a datapoint in a consecutive set of datapoints deviates extremely from previous points, the next datapoint has a higher chance of being closer to the mean.

Galton created a simple experiment to prove the regression to the mean, which we now call a Galton Board. The Galton Board contains a funnel with balls and nails in an evenly distributed fashion, as shown in the figure below.

It doesn’t matter how often you repeat this experiment. The balls will always fall and depicture a normal distribution in the channels at the bottom.

That’s because, for every single ball, there is a 50/50 chance that it will fall one way or the other. The odds of a ball constantly hitting to the right and ending up on the very right side is considerably less than for the ball traveling to the middle.

In financial terms, this means that in the short term, the price can fluctuate extremely to the up- or downside. Over the long term, the fundamental characteristics and economic environment dictate the company’s growth trajectory.

The Strongest Force in the Stock Market

I state that the regression to the mean is one of the strongest forces in the stock market. I’ve closely followed the stock market for 6 years and studied its 400-year history.

Over the long run, the stock market’s growth is tightly coupled with the country’s growth trajectory. There are major up- and downswings, but the stock price tracks the company’s fundamentals over the long term.

The charts below show the stock price, revenue, and price-to-sales ratio of Peloton, Palantir, and Crowdstrike. In 2021, all three experienced a major upswing in valuation. Price to sales ratios reached 15, 48, and 60 for the stocks, respectively. These valuations were major deviations from their historical means.

Each company is growing exceptionally well in its respective industry. But exaggeration, speculation, and the lockdown led to valuations that could not justify any intrinsic growth projections.

The reverse is also true when the stock price deviates strongly to the downside even though the company’s business remains fundamentally strong. Investors buying stocks against the market mood are often called contrarian investors.

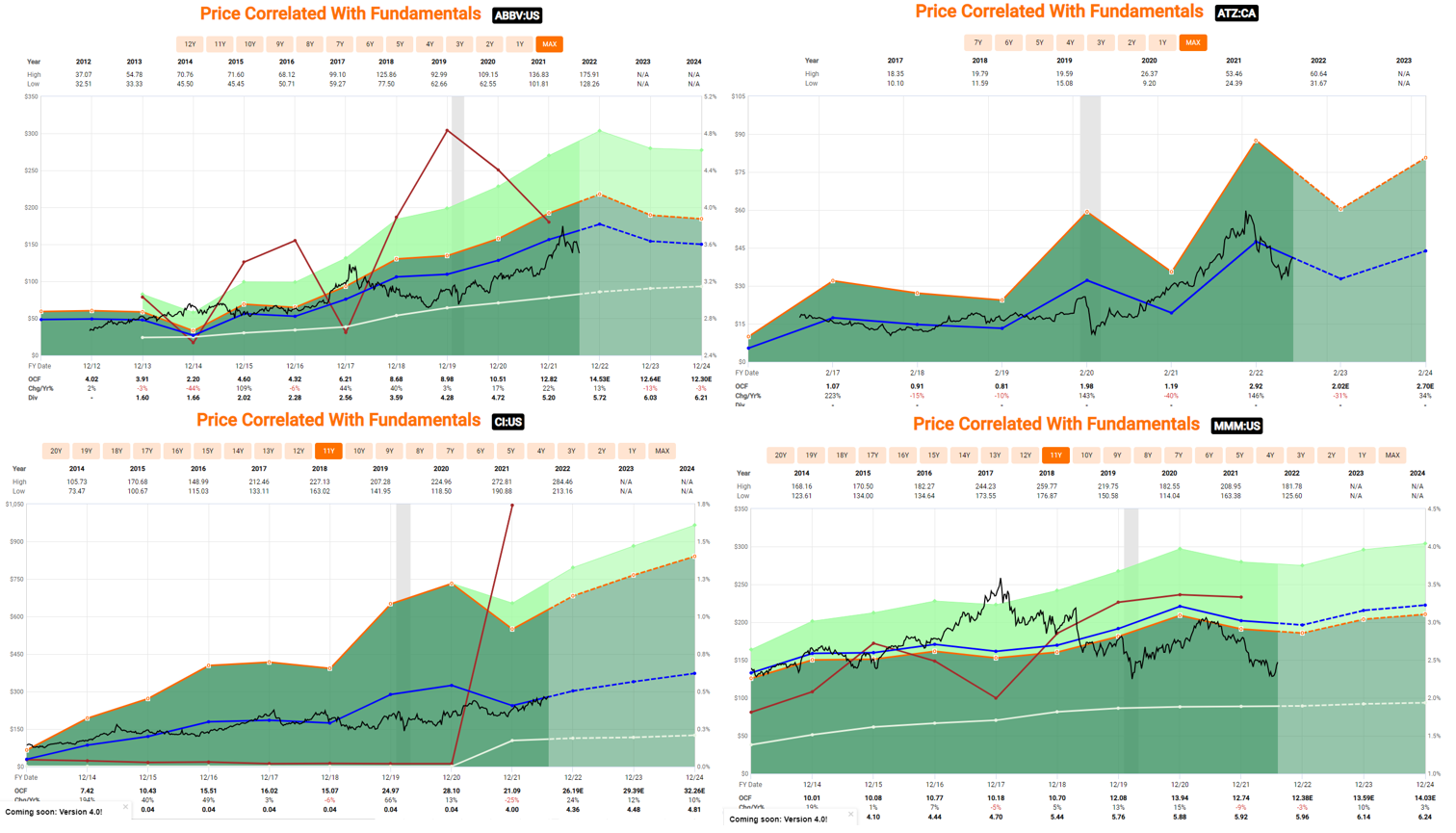

Here are 4 companies that reversed to the mean on the upside. On the top left is Abbvie, which has been growing operating cash flow consistently but fell out of the investor’s favor in 2018. Valuation caught up with fundamentals, and investors who would have bought at the lows in 2018, would have enjoyed a 33.8% annual rate of return.

Same story with Cigna. It experienced a low during 2018. Contrarian investors have enjoyed a 23.1% annual rate of return since then.

3M is currently in one of its downtrends due to lawsuits and environmental challenges. 3M’s growth rate has been rock solid for decades and yet, experienced many swings. Each time, it reversed back to the mean. The question this time - Will the regression to the mean be powerful enough to do the same this time?

The last one in this example is Aritzia, an apparel company experiencing the power of the regression to the means in full force.

What can you, as an Investor, do?

Knowing the regression to the mean is already the first step towards salvation. That was a bit poetic, but you get the point. Companies and industries are characterized by long-term trends with characteristic growth rates that depend on present and future demand.

Anticipating these growth rates is no easy task but having a long-term mindset is enormously helpful. Many research firms calculate and estimate growth rates for various industries and applications. Use these as your base case.

Don’t fall for other cognitive biases like confirmation biases or the illusory truth effect. On Twitter, it’s easy to fall victim to Echo Chambers, which tells you exactly what you want to hear. Listen to counterarguments and take them seriously!

Look at the valuation metrics! Valuation metrics are always relative. No ONE number is good or bad. But looking at a company’s historical valuation metrics is a good yardstick. If the company’s valuation deviates strongly from its historical mean without the fundamentals having changed, look closer to if there is an opportunity (downside) or reason for pausing your Dollar-Cost-Averaging situation for a while (upside).

Conclusion

2022 and the regression to the mean taught many people humility. That’s clearly observable on Twitter. Here is a little collage about the Peloton stock from 2020/2021 when valuation and irrationalism were at their peak.

These people are either now barely active on Twitter or completely changed their tweeting and investing style. Regression to the mean is a ruthless teacher.

Valuation matters!

Over the short-term or long-term, valuation matters in either case. The best company in the world that’s trading way above its historical valuation can underperform a mediocre company that’s severely undervalued.

Having a long-term mindset dissipates some of the risks of overvaluation because the investor averages into the stock, but it doesn’t completely de-risk it. Investors can drastically improve their returns with attention to valuation and business metrics.

I always welcome constructive criticism and open discussions. Please feel free to comment or PM me about my calculations and/or sources that I use in my articles.