Jeff Bezos - 24 Shareholder Letters with 24 Lessons - 2004-2008 - Part 2

Jeff Bezos - 24 Shareholder Letters with 24 Lessons - 2004-2008 - Part 2

The years 2004-2008 were mission-critical and life changing years for the global economy. During these years, Jeff Bezos explained in detail his most important financial metric - Free Cash Flow

In 2021, Jeff Bezos’s tenure as CEO of Amazon ended. Luckily, he left us with 24 extremely insightful shareholder letters. In these letters, Bezos talks about Amazon, becoming a successful businessman/woman, a better investor, and how he looks at work as a whole.

During 2004-2008, Bezos discusses his favorite financial metric - Free Cash Flow, decision-making principles, and how delaying gratification leads to superior investment returns and business success.

If you haven’t already or need a refresher on the years 1997-2003, read my previous article here.

2004 Shareholder Letter - Free Cash Flow, the Ultimate Financial Measure for Amazon!

Bezos goes into detail about cash flow, its properties, and how to think about free cash flow when investing. It's practically a finance 101 class for free in this shareholder letter.

Key Learning: Shares represent the present value of their future cash flows and not the present value of their future earnings. Earnings do not translate on their own into cash flows. Earnings, working capital, capital expenditures, and future share dilution are important components of cash flow.

Bezos provides a detailed case study to support his argument.

A transportation company transports people from A to B with a futuristic teleportation machine. The machine is expensive ($160mn) with an annual capacity of 100,000 passenger trips and four years of useful life. Each trip costs $1,000 and requires $450 in COGS and $50 in labor and other costs.

In Year 1, the machine was fully utilized, which led to earnings of $10mn - a 10% net margin. The entrepreneur decides to invest more capital and adds machines in Years 2 through 4.

If investors only look at earnings, the company seems to do very well, doubling earnings each year. But looking at free cash flow, the picture looks different, with a cumulative negative free cash flow over four years of $530mn.

EBITDA paints a similarly faulty picture of the health of the company. Without including the capital expenditure of the machines, it looks like EBITDA is doubling each year. Reducing the Capex for the machines shows that the company would burn cash.

This transportation company is fundamentally flawed. The income generated by the machine doesn't justify the cost of the machine. No sane investor would invest money in this business.

For Amazon, the financial focus is on long-term growth in free cash flow per share.

2005 Shareholder Letter - Decision-Making

How does Amazon make decisions? Bezos discusses in detail the decision-making process at Amazon based on empirical and scientific research.

Amazon's decision-making process is based on data. There is no black and white in decision-making. It's always a balance between better and worse answers.

There is a limit to how many decisions a company can make solely based on data. Decision-making related to growth and innovation requires another important variable - judgment. At this point, I'd like to cite Bezos:

"We cannot numerically estimate the effect that consistently lowering prices will have on our business over five, ten, or more years. Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long term to a much larger amount of FCF and a more valuable Amazon.com"

Key Learning: Math-based decision-making is cheered upon, but judgment-based decision-making, often debated and controversial, leads to innovation and creates long-term value.

Good judgement comes from experience, and a lot of that comes from bad judgement.

Will Rogers

For example, letting third-party sellers on Amazon's marketplace seemed like a crazy idea at first. Why should a company invite competitors and allow them to outbid them on its platform? Bezos and Amazon judged that a larger marketplace makes customers happier, allowing them to have more and better choices. It would be tough for Amazon as it lost business to competitors in the short term. In the long term, this strategy attracted more customers to the platform. In 2005, 28% of marketplace sales were from third parties, compared to 6% in 2000. In 2021, 61% of GMV comes from third-party sellers.

Shareholder Letter 2006 - Differentiate Yourself

Key Learning: Bezos invests in areas that allow him to differentiate himself and require low capital investments with high returns. If there is no differentiation factor or competitive advantage, it's a business Amazon doesn't invest in because it doesn’t know how to improve and play its strength.

This is exactly why Amazon never had any physical stores. Bezos said the following about opening stores: "We don't know how to do it with low capital and high returns."

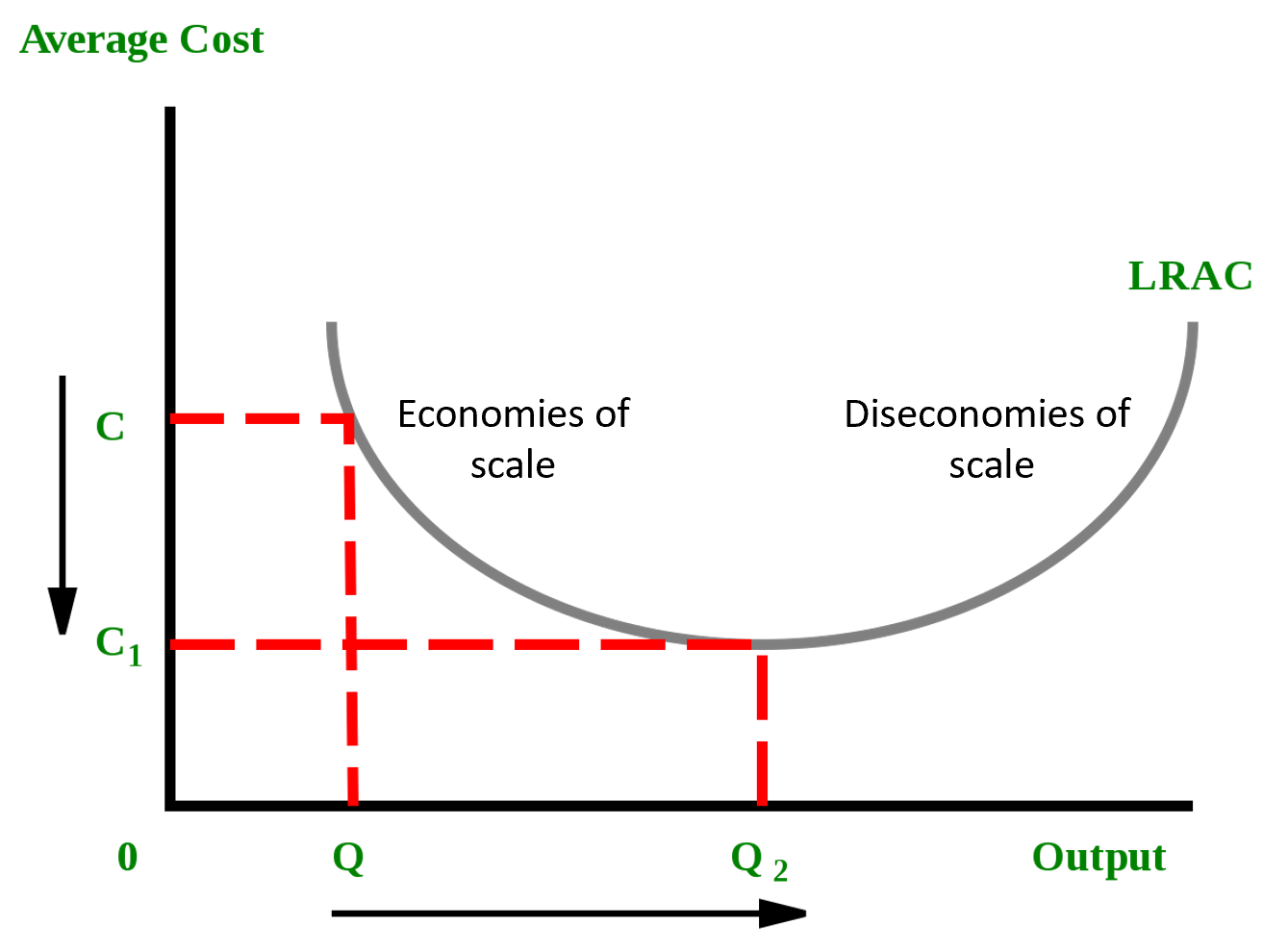

Amazon's leverage is its fulfillment center network around the globe. These are connected centers that track inventory and allow web services - APIs - to track everything happening inside the warehouses. The cost to store inside Amazon's warehouses is 45 cents/cubic foot (in 2006). By storing inside Amazon's warehouse, customers have access to all APIs, packaging, and tracking services inside these warehouses. Amazon is still at the beginning of the economies of scale graph before it reaches the point where any additional warehouse would lead to a diseconomy of scale.

Amazon created a differentiated logistics and warehousing business that works mostly autonomously.

This is the first time Bezos mentioned Amazon Web Service in his letters. Amazon builds a network around its logistics centers and allows others to use it. The primary consumers of these networks are developers that need storage and compute capacity. Contrary to how Amazon's competitors handle cloud computing requests, Amazon created an on-demand cloud computing platform and APIs. Instead of forcing the customer to buy a set computing and storage amount, Amazon allows pay per use.

2007 Shareholder Letter - The year of the Kindle

The Kindle is a library in people's pockets. The Kindle shows that Amazon is not bound to a sector or industry. Bezos emphasizes that when he and his innovators find business potential with low capital investments and high returns, and a differentiated way to create a competitive position, they will invest and enter the market.

The Kindle is a prime example. It doesn't compete with books but adds new capabilities that are not possible with traditional books. Amazon never intended to copy the book or copy bookstores with Amazon.com. Amazon made book shopping more convenient, allowed others to write reviews, and added a new information layer that is impossible in traditional bookstores.

Key Learning: Look for what kind of businesses a new platform enables a company to realize, how scalable it is, and what industries it could potentially disrupt.

Paradoxically, the Kindle is not about the hardware itself but about the window of opportunity it opens to its users and creators. Putting a Kindle in everyone's hands allows Amazon to offer unique and scalable publishing services.

The Kindle allows people to carry thousands of books in a small and uninteresting form factor in which you'd forget to hold a device in your hand and focus on what you're reading.

Kindle is a reinvention of a book.

2008 Shareholder Letter - The Financial Crisis

Bezos's response to share shareholders in the financial crisis is "The long term goal and fundamental approach of Amazon doesn't change during these times."

Humans are instant gratification seeking, which is why many don't seem to reach their long-term goals in life and run from one endorphin rush to another. Amazon is different. Because long-term thinking is engrained in Amazon's philosophy, they can plant new project seeds for years without hasting them - this way, Amazon identifies evolving customer needs and develops and delivers solutions for them.

Key Lesson: Long-term investors achieve the highest returns by delaying gratifications. Another key aspect is avoiding the craving to react and be unnecessarily active. Long-term investing is called long-term because its thesis requires time to evolve.

Bezos differentiates between "Working Backwards" and "Skills-forward."

Skills-forward means that companies look at their current skills and ask, "Where else can our company deploy these skills?" The problem with this approach is that the company doesn't evolve new skills but looks to redeploy its current skillset.

Working backward from customer needs demands a company to evolve new competencies and skills that, at first, seem unnatural and weird, but with training and diligence, become unique competitive advantages to the company.

The Kindle is an excellent example of how Amazon works backward and builds new skills in hardware development to enable creators and readers to share a platform.

2008 is also when Bezos first mentioned Amazon Prime in his letter. Prime is an offer that saves customers worldwide $800mn in shipping alone.

Conclusion

I hope you enjoyed this week’s article on Bezos’s 2004-2008 shareholder letters. Next week I’ll release the next few year’s summary and key learnings!

Here is the link to the previous article for the years 1997-2003.

If you liked this article, please like and share it with others.