Jeff Bezos - 24 Shareholder Letters with 24 Lessons - Part 1

Jeff Bezos wrote 24 shareholder letters in which he shared Amazon's strategy, his insights, and his way of thinking with his shareholders and the public. He describes lessons he learned throughout his

This series of articles will discuss the 24 shareholder letters that Jeff Bezos published during his tenure as CEO of Amazon.

Summary

1997 and 1998 lay the foundation for the next few years. Bezos is famous for being a long-term thinker and teaches us how to become one too.

1999 and 2000 are fascinating years, as Amazon is growing and creating substantial economies of scale exactly before the DotCom bubble bursts.

2001 and 2002 are all about building and maintaining competitive advantages. These years provide critical information for investors and business people.

2003 discusses what true ownership looks like and why investors should rather act as owners than renters of companies.

1997 Shareholder Letter - Think Long Term

Probably the most known and seen shareholder letter in the world. Bezos has been attaching this letter to each following shareholder letter. The key message Bezos makes here is:

It's all about the long term!

Bezos and Amazon have the privilege to concern themselves thinking decades ahead in creating shareholder value. They can invest in new business segments, adjust them, and grow them to massive scales through trial and error.

The three most important metrics to increase the return on invested capital are customer growth, revenue growth, and the brand's strength.

The only way to accomplish this is to become the market leader, which translates into higher revenue and profitability, greater capital velocity, and better returns on invested capital.

Bezos lays the foundation for Amazon to become a customer-obsessed company.

1998 Shareholder Letter - Competitive Advantage

After expanding to the UK and Germany, Amazon's sales increased 4-fold, and it became the leading online bookseller in these markets. 25% of Amazon's revenue now comes from new businesses in Germany, and the UK, the sale of music, video, and gift cards.

In 1998 Amazon introduced the 1-click button, gift button, store-wide sales rankings, and instant recommendations.

I find the passage discussing the sales ranking and instant recommendation fascinating as it is the very beginning of Amazon's data-focused platform. They're integrating the customer information in real-time into their website, creating probably the biggest competitive advantage of the internet era.

Amazon is a cash-favored and capital-efficient business. Cash favored means that Amazon's business is scalable. Amazon doesn't need physical stores in town; it needs central logistics centers that can carry millions of items. The ratio of the area of a logistics center to the addressable consumer is much higher than the ratio of a physical store to addressable consumers. This ratio shows itself through Amazon's inventory + equipment turnover, which was ~17 in 1998. Removing equipment from the equation, Amazon's inventory turnover is 32! Compare that to supermarkets with a ratio between 6-10 and grocery markets with 4-8.

Key Learning: Companies need a competitive advantage to build their business; otherwise, they will be drawn to mediocrity and mediocre returns for investors.

The axiom on which Bezos build Amazon is "Customers are perceptive and smart. Brand image follows reality and not the other way around." Amazon focuses relentlessly on customer satisfaction, ease of use, customer experience, and relationship.

Key Learning: Customers are loyal until someone else offers them a better service!

Maintaining customer loyalty with an offering too good to turn down is a competitive advantage.

1999 Shareholder Letter - The Tipping Point

This year, Amazon's sales broke the billion-dollar barrier. Its sales grew from $610mn to $1.6bn, and it added 10.7mn customers, which is an increase from 6.2mn to 16.9mn.

In 1997, 100% of Amazon's sales came from books. In 1999, 50% of sales were from books, and the rest distributes on Auction, zShops, toys, consumer electronics, home improvement, software, video games, payments, and Amazon Anywhere.

Amazon is scaling up rapidly in areas where scale matter and creates a competitive advantage. It increased distribution capacity from 300,000 sqft to 5mn sqft in the last 12 months. Increasing distribution capacity allows Amazon to address disproportionally more customers with each square feet capacity.

Amazon processes $2bn in sales but requires only $220mn in inventory and $318mn in fixed assets. Its inventory turnover remains >16.

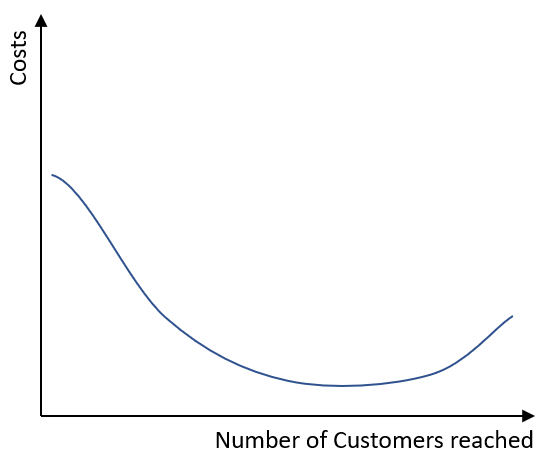

There is a non-linear relationship between the costs to scale Amazon's logistics network and the number of customers reached. At this point, Amazon is at the beginning of the graph. It has a lot of room to grow and reach more people in the US.

In 1999, Bezos talked about a "tipping point" where Amazon is reaching a scale where it can launch e-commerce businesses faster, with a higher quality of customer experience, low incremental costs, a higher chance of success, and a faster path to scale and profitability than any other company. It is the beginning of Amazon's marketplace, where it realizes that it can create disproportionate more value for customers by allowing third-party sellers to sell on the platform.

Key Learning: Expand your scale and put customer satisfaction and experience before short-term benefits for your revenue or margins.

The main focus points of Amazon remain increasing customers, strengthening customer relationships, increasing the number of products, the frequency with which customers shop, and the level of satisfaction they have. These points result in better brand awareness, better customer service, and better distribution.

2000 Shareholder Letter - Popping Internet Bubble

Amazon's share price had dropped 80% by the time of writing. Bezos remains unfazed, and his focus on the long term reflects itself right in the beginning by quoting the godfather of value investing, Graham:

"In the short term, the stock market is a voting machine, in the long term, it's a weighing machine."

- Benjamin Graham

Amazon's fundamentals remain extremely strong, with all key metrics increasing. This year, Bezos reflects on the bursting dot.com bubble and especially on companies like pets.com and living.com. He is not concerned with the decline in Amazon's stock price.

Key Learning: These e-commerce businesses were single-category e-commerce companies. Reaching the required scale to become cash-flow positive requires much longer than for multi-category e-commerce businesses.

Online selling is s scale business characterized by high fixed costs and relatively low variable costs, which is why small and medium-sized e-commerce businesses have it rough.

The foundation of Amazon Web Services

Bezos specifically discusses Moore's law, and I have the feeling that it's this year that lays the foundation for Amazon Web Services. He knows that the price-performance for processing power doubles every 18 months, disk space every 12 months, and bandwidth every nine months.

2001 Shareholder Letter - Amazon's Three Pillars

In November 2000, Amazon launched one of its most iconic products - Amazon Marketplace. Bezos indirectly described the Marketplace in 1998, 1999, and 2000 by discussing how scale matters in the e-commerce business and how central logistics hubs reach disproportionately more customers. Amazon Marketplace allows third-party sellers to sell their products on Amazon and optionally use its logistics capabilities to send the packages. It's the beginning of mass online retail adoption.

Amazon Marketplace made up 15% of its US business within the first year.

Amazon's Three Pillars - Something we take for granted nowadays

Product Selection <> Convenience <> Lower Prices

Amazon's growth and scale allow it to share cost efficiencies with its customers, provide major discounts on books, and offer free shipping on orders over $99. Amazon's growth is spreading the high fixed costs rapidly.

Important for Investors - Bezos' single best metric to evaluate a company - Free Cash Flow

"A share of a stock is a share of a company's future cash flow."

If an investor could only know two things about a company, its future cash flows and the number of outstanding shares, you could reasonably well estimate the business's fair value.

Key Learning: An investor can make reasonable estimates about a company's future cash flows by looking at past performance and examining leverage points and the scalability of the company's business model. For example, Amazon has high fixed costs for delivery and inventory, which means that increasing customers will substantially affect free cash flow generation.

2002 Shareholder Letter - Measuring Effectiveness

Logistics and inventory management are two important competitive advantages that Amazon created. When assessing Amazon's ability to provide the best customer experience, the two best metrics are cycle time (amount of time taken by the fulfillment center to process an order) and contact per order (customer satisfaction).

Inventory turned over 19 times in 2002. An amazing feat. That means that Amazon can satisfy $19bn of customer orders with only $1bn in inventory.

Amazon transfers these efficiencies to customers as lower prices for many goods.

Key Learning: Companies must be able to measure their effectiveness and competitive advantage within an industry. A competitive advantage must result in metrics that are at the top of an industry.

This year, Bezos showed the power of fixed expenses. He compares Amazon to super-book-stores in Seattle and NYC. If you'd buy the 100 best-selling books in the stores, you'd pay $1561; at Amazon, they cost $1195. In the stores, 15 out of 100 books were discounted. At Amazon, 76 of 100 were discounted.

2003 Shareholder Letter - True Ownership

Long-term thinking is a requirement and the result of true ownership. Bezos discusses how owners fundamentally differ from tenants by comparing how they take care of their things.

Important Lesson for Investors

Many investors are effectively short-term investors or tenants who shuffle their portfolios so quickly that they are just renting the stocks they temporarily "own." Bezos's statement reminds me a lot of the book 100 Beggars. Investors crave activity. Social media feeds it further, with people sharing the newest (mostly irrelevant for the long term) information on Twitter, Facebook, or the News. Instead, investors interested in investing in 100 Beggars should concern themselves with ideas that could become big. Compare the size of the opportunity in the future with the company's size now.

Long-term thinking and brutal customer focus are the most important aspects of an investment's ownership and success. Bezos discusses customer reviews on Amazon. Amazon posts everything, positive and negative reviews on products. It could only show positive reviews and make more money in the short term, but customers would realize that the product is shit in the long term, which would hurt the company's future earnings.

The most important distinctive competitive advantage remains the price. Customers love low prices, and to provide them with that, Amazon eliminates defects, improves productivity, and passes those results to the customer.

Conclusion

In the next article, I'll provide the key lessons of the next few years. There are so many things to learn from Bezos's shareholder letters, not only for its shareholders, but for investors, business people, and individuals.

The next years are fascinating. We'll learn about the value of free cash flow, the importance of decision-making, and learn to categorize decision-making into different baskets.

Feedback is always welcome!